Track healthcare's 2026 setup: GLP-1 drug adoption, a valuation gap vs. tech, and why VHT offers broad exposure with low fees and... ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ |

| | Written by Jordan Chussler

With well-publicized losses for companies including UnitedHealth Group (NYSE: UNH), Elevance Health (NYSE: ELV), and Wegovy and Ozempic maker Novo Nordisk (NYSE: NVO), the healthcare sector failed to outperform the broad market last year. In the three years prior to that, the sector finished with gains of just 2.6% in 2024 and 2.1% in 2023, and a loss of 2.0% in 2022. But healthcare stocks have appeared to turn a corner. Over the past six months, the sector—which enjoys inelastic demand—has led all 11 sectors of the S&P 500 with a nearly 19% gain. According to investment professionals, the trend that began in mid-2025 is likely to continue into the new year. For shareholders of the Vanguard Health Care ETF (NYSEARCA: VHT), that is already proving to be true. 2 Major Catalysts for the Health Care Sector There are two major tailwinds that should help health stocks continue to enjoy this bullish momentum. One—the mass adoption of weight loss drugs—was partly responsible for the sector’s bullish reversal halfway through 2025. The other—comparatively low valuations—could continue to attract inflows as investors look to lock in profits and hedge against positions that present more inherent volatility. America’s Weight Loss Treatment Craze Weight loss treatments including GLP-1 agnostics and semaglutide treatments such as Novo Nordisk’s products Ozempic as Wegovy are becoming widely adopted. At the same time, pharmaceutical companies are shifting from injectable treatments to pill form, while others, like Pfizer (NYSE: PFE), are doubling down on their investments in the weight loss market. Speaking on the popularity of these drugs, Catherine Brown, vice president of clinical services at digital health firm Welldo, recently told Reuters that “We're imagining these medications may become so common that everybody's got a GLP-1 app ... right there on your phone next to your bank account." Forecasts from industry consultancy firm Grand View Research indicate that the GLP-1 drug market could grow by a compound annual growth rate of 18.54% between 2024 and 2030, resulting in a global market value increase from $13.84 to $48.84 billion. Low Healthcare Stock Valuations Are Attracting Inflows In the wake of President Trump’s tariff announcements in April 2025—trade policies that have had an adverse effect on imported pharmaceuticals—stocks operating in the health care sector have experienced almost comically low valuations, particularly when juxtaposed with the historically high valuations of tech and communication services stocks. Pfizer, for example, sports a trailing 12-month (TTM) price-to-earnings (P/E) ratio of 14.7, while Health benefits provider Elevance and Johnson & Johnson (NYSE: JNJ) have P/E multiples of 15.32 and 19.86, respectively. For context, tech favorites such as Palantir (NASDAQ: PLTR) and Tesla (NASDAQ: TSLA) have TTM P/E multiples of 421.11 and 290.53, respectively. In turn, it was only a matter of time until health care’s ratios caught the eye of value investors looking for opportunities at the tail end of 2025 and heading into 2026. In November 2025, Mizuho’s healthcare equity strategist Jared Holz told Barron’s that “When you see money come out of a space, especially one that’s filled with trillion-dollar [tech] companies, it really doesn’t take much to get some of the underperforming sectors a little juice.” Vanguard’s VHT: A Basket of Undervalued Stocks The Vanguard Health Care ETF is up 2.30% this year after gaining more than 18% over the past six months. Much of those gains were fueled by rebounds and strong end-of-year performances from the fund’s top holdings. Those positions include the ETF's top five holdings: Eli Lilly (NYSE: LLY), AbbVie (NYSE: ABBV), Johnson & Johnson, UnitedHealth, and Merck (NYSE: MRK). Drilling down further into the holdings, VHT also has allocations to Pfizer, CVS Health (NYSE: CVS), which acquired health insurance giant Aetna on Nov. 28, 2018, and the United States’ largest hospital chain HCA Healthcare (NYSE: HCA). The ETF carries a negligible expense ratio of 0.09% while paying a dividend that currently yields 1.58%, or $4.64 per share annually. What Wall Street Thinks About VHT Based on analysts’ ratings of 23 companies in the VHT portfolio (64.3% of its total), the fund receives a Moderate Buy rating. Perhaps the strongest indication of Wall Street’s enthusiasm about the health care sector is the ETF’s current short interest of just 0.33% of the float, or less than 195,000 shares of the 60.17 million shares outstanding. That marks a nearly 37% decrease in short interest since the last reporting period.  Read This Story Online Read This Story Online |  REVEALED: America just unlocked a $500 trillion asset

Everyone's talking about AI stocks but almost no one is talking about what AI actually runs on.

Nickel. Copper. Cobalt. Manganese.

America just secured exclusive rights to the largest untapped supply on Earth.

One company is already in position and this could be one of the most important AI infrastructure plays heading into 2026. The name and ticker are available here now >>> |

| Written by Dan Schmidt

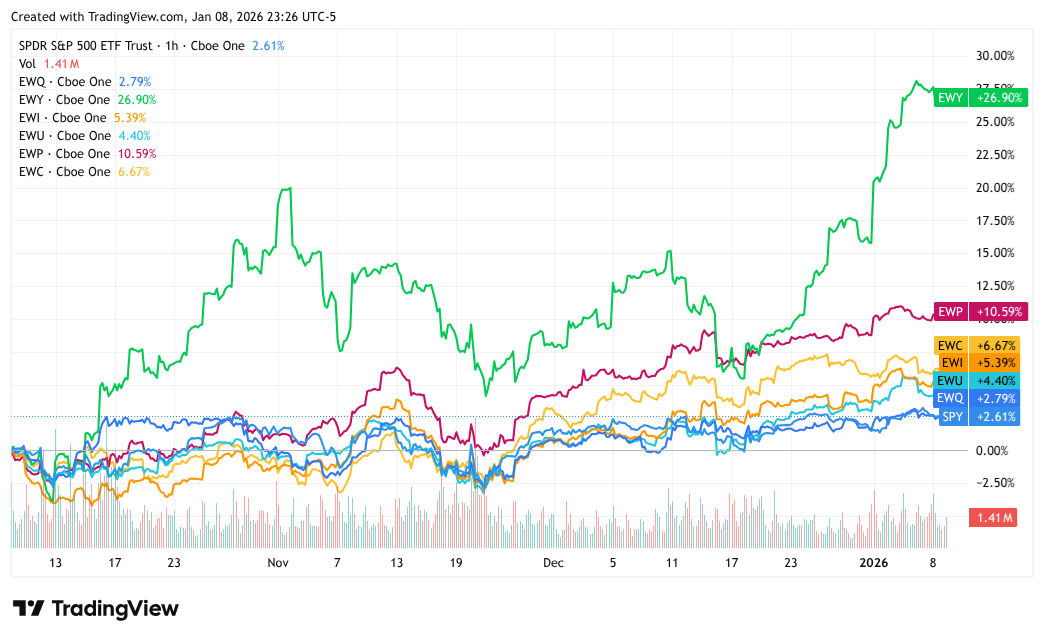

What were the best-performing sectors and industries in 2025? For most investors, some version of tech need for AI is the answer, whether it's semiconductors, memory storage, or software. It could be a commodities-based industry, such as gold or silver. A mention of international bank stocks might raise eyebrows, but this sector deserves to be mentioned in the same breath as the rest of 2025’s winners. Global banks, especially European ones, enjoyed tremendous outperformance last year, thanks to several tailwinds from both home and abroad. Can these tailwinds continue in 2026? Two international bank stocks appear well-positioned to deliver additional upside as favorable trends remain in place. International Stocks Continue to Outperform U.S. Peers Despite a resurgent artificial intelligence trade in the U.S., the fourth quarter of 2025 was another win for its international peers. The SDPR S&P 500 ETF (NYSEARCA: SPY) has gained 2.61% over the last three months, but that gain was more than doubled by ETFs representing equities in Italy, Canada, Spain, and South Korea. South Korean equities are on a particular tear, surging nearly 27% since the start of October. The tech sector has done much of the lifting in the U.S. markets over the last few years, while international markets have become more diverse and less expensive.

The outperformance of international equities continues to be led by many of the same influences. The US dollar is no longer free-falling versus other currencies, but it remains weak against majors like the Euro and British pound. Currency pressure is also highlighting the valuation disparity between U.S. and international equities. While the price-to-earnings (P/E) of the S&P 500 continues to drift toward 30, European and Canadian indices are sitting at more modest P/Es between 17 and 20. The banking sector in these countries is particularly undervalued, with P/Es often between 10 and 12. International banks also tend to be more friendly with dividends than their U.S. counterparts. Public U.S. banks often prefer buybacks to dividends when returning value to shareholders, which can be more tax-friendly, but also doesn’t help an investor seeking steady income from their portfolio. International banks frequently yield higher dividends than those of typical large-cap domestic banks. Few Sectors Have Been Hotter Than International Banking: These 2 Stocks Lead the Pack The banking sector of the European Stoxx 600 index has actually outperformed the U.S. tech sector since 2021, yet valuations remain suppressed. If you’re looking to diversify your portfolio away from tech-heavy U.S. stock indices, consider one of these international bank stocks that offer value and outperformance potential. Deutsche Bank: No Longer the Sick Bank of Europe For many years, investors avoided shares of Deutsche Bank AG (NYSE: DB) like the Dallas Cowboys avoid playoff victories. If there were a scandal in European banking, it was a good bet Deutsche would have a hand in it, and fines and restructuring costs kept the stock in a steady decline following the 2008 financial crisis. DB shares are still far off their 2007 all-time high, but the stock is up 500% since July 2022 thanks to a series of cost-cutting measures designed to exit underperforming businesses and return to core strength areas (and profitability).

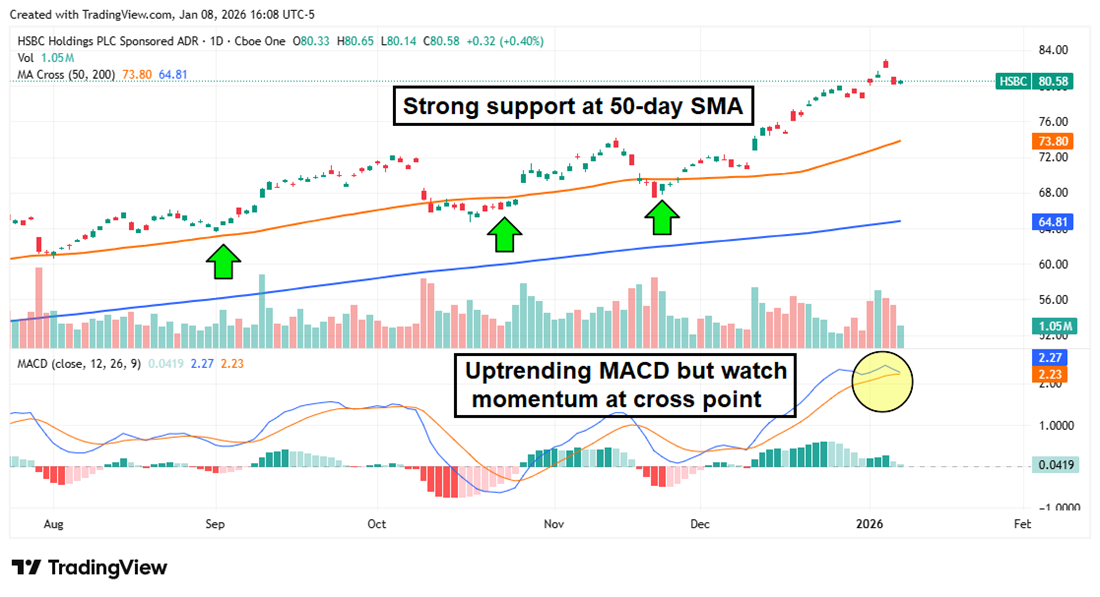

Probability has been delivered to DB shareholders: three straight quarters of positive EPS figures and three massive revenue beats. Despite strong earnings, the stock trades at just 13 x forward earnings and 0.87 times book value. Deutsche Bank no longer needs to be handled with gloves, and the chart shows a bullish trend with plenty of momentum behind it. The 50-day simple moving average (SMA) was a great entry point for investors in 2025, and it appears to be holding strong into the new year. HSBC Holdings: Bridging Europe and Asia HSBC Holdings plc (NYSE: HSBC) is in a unique position as a large-cap bank with significant ties to both Europe and Asia. The company is doubling down on Asia, having recently acquired and privatized Hang Seng Bank to leverage its footprint in Hong Kong. HSBC’s wealth management operations in Asia are also scaling quickly, giving the bank ample sources of both fee revenue and interest income. HSBC is a responsible capital steward, paying a 2.46% dividend yield with a 41% payout ratio. It also rewarded shareholders with a special dividend and share buybacks, using the cash from selling its Canadian banking units.

A strong dividend and a growing global client base offer opportunities for income and stock price appreciation, and analysts spent much of Q4 2025 upgrading HSBC. Zacks Research, Erste Group Bank, Bank of America, and Keefe, Bruyette and Woods all upgraded the stock to Buy or Strong Buy before the end of the year. HSBC shares have soared nearly 20% in the last three months, so investors must watch the MACD for signs of a pullback. The 50-day SMA is once again an ideal entry point should momentum wane from here. Read This Story Online |  Everyone's buying Nvidia. The financial media can't stop talking about it. Your neighbor probably owns it.

That's exactly why I'm looking elsewhere.

See, when everyone piles into the same trade, the easy money is already gone. The real profits come from finding what the crowd is missing. Click here to get your free copy of this report |

| Written by Ryan Hasson

Over the past 12 months, the U.S. dollar has weakened meaningfully, and with additional rate cuts still on the horizon, that trend may persist against several major emerging-market currencies. That shift has helped fuel a strong rally across emerging market equities, with the iShares MSCI Emerging Markets ETF (NYSEARCA: EEM) surging over 34% over the last year. While pullbacks within any broader trend are inevitable, continued dollar weakness could further encourage capital rotation into emerging markets as U.S. investors look to diversify beyond domestic equities. For broad exposure, EEM remains one of the most widely used and liquid vehicles for accessing this theme. The ETF tracks the MSCI Emerging Markets Index, providing exposure to large- and mid-cap equities across countries such as China, Taiwan, India, Brazil, and South Korea. It also offers a modest income component, with a dividend yield of 2.1%. Institutional positioning suggests confidence in the trend as well, with roughly $5.5 billion in inflows over the past twelve months versus $3 billion in outflows. While EEM is well-suited for investors seeking diversified exposure, some may look for a more aggressive way to express a bullish view on emerging markets. That often means concentrating on individual stocks rather than relying solely on an ETF. One name in particular, which carries a 3.16% weighting in EEM, stands out particularly for its technical positioning. Alibaba: A Potential Emerging Markets Leader Alibaba Group Holding (NYSE: BABA) remains one of the most influential companies within the emerging markets universe. The Chinese multinational technology and e-commerce giant commands a market capitalization of roughly $368 billion and plays a central role across online retail, cloud computing, logistics, and digital payments. From a technical standpoint, BABA is presenting a compelling setup. After breaking out to new 52-week highs last September, the stock pulled back in a controlled and constructive manner. Importantly, shares found support near the $150 area, which previously acted as resistance. That successful retest suggests the stock may be attempting to form a higher low within a developing longer-term uptrend. A sustained move above $160 would likely confirm the next leg higher and could attract renewed momentum-driven flows, particularly if emerging markets continue to outperform broadly. Fundamentally, valuation remains reasonable relative to Alibaba’s scale and long-term growth profile. The stock trades at 21 times earnings, with a forward P/E near 17. Analysts remain bullish, with a consensus price target of $191.84, implying 24% upside from current levels. Institutional flows, however, tell a more nuanced story. During the third quarter of last year, institutions were net sellers, unloading $29 billion in stock versus just under $4 billion in buying. Much of that selling came after a sharp rally from March lows near $80 to a September peak just below $193, suggesting profit-taking rather than a significant fundamental shift in outlook. The key question now is whether capital will begin to rotate back into the name if emerging-market momentum remains intact. AI and Cloud as the Next Catalyst One potential catalyst lies in Alibaba’s expanding AI and cloud initiatives. Recent reports indicating that select Chinese companies, including Alibaba, may gain access to NVIDIA’s H200 chips for commercial use could provide a meaningful tailwind. While Alibaba’s core e-commerce business has faced pressure from discount-focused competitors, its AI-driven cloud segment continues to grow rapidly. Alibaba Cloud controls nearly one-third of China’s AI cloud market, and the company has committed over $50 billion over the next three years toward cloud and AI infrastructure. If emerging markets continue to attract capital, and if Alibaba can reclaim and hold above key technical levels, the stock appears well-positioned to lead the next phase of outperformance within the space, potentially. Read This Story Online |  |

|

| |

|

|