With EA likely going private in a $55-billion deal, opportunities may arise for other gaming companies. Here are some considerations for... ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ |

| | Written by Nathan Reiff

Major video game publishing firm Electronic Arts Inc. (NASDAQ: EA), known for franchises including FIFA and Battlefield, drew headlines in late September when it announced it would be acquired in an all-cash deal worth a whopping $55 billion. The investor consortium acquiring the company, which includes Silver Lake, Affinity Partners, and the Saudi government's sovereign wealth fund, plans to take EA private. Meanwhile, investors face key questions: how should they respond to the recent news from EA before the acquisition is finalized? What does this development suggest for the wider video game industry, a giant that, despite recent slower growth and tempered consumer spending, still has a global valuation of nearly $500 billion? In the short term, continuing to hold shares of EA may be the optimal move for most prior investors, as the company's stock spiked following the acquisition announcement. Shares are trading up 19% in the last month but have plateaued so far in October. For investors, the greater opportunity may actually lie in alternatives like Take-Two Interactive Software Inc. (NASDAQ: TTWO) and Roblox Corp. (NYSE: RBLX), although some caution is warranted as the video game industry shifts. What Might Happen to EA Shares While Awaiting Acquisition? The EA deal announcement was a boon for investors already holding stock in the company, with the value of the deal placing a sizable premium of about 17% on the share price even at its highest point earlier this summer. Of course, the potential for new investors in EA to win gains in the acquisition is mostly nil at this point, as the price of EA stock quickly shot up above $200 to new all-time highs after the news broke. Buying shares of EA now—unless there's an unusual blip in the price and it drops before the acquisition is finalized—is not likely to generate much by way of returns for investors. There has, on the other hand, emerged a contingent of investors willing to bet against EA stock and, potentially, the acquisition itself. These investors have contributed to a growing short position in recent weeks: short interest has climbed by almost 13% in the last month. This is a risky bet as well, as it seems highly likely the deal will close despite a 45-day window for other offers to emerge. Implications for the Broader Gaming Industry EA's reliance on in-game microtransactions and other controversial game mechanics has drawn ire from customers in the past and even prompted a European investigation into whether some of the features of EA games might constitute gambling. These same customers may see the company's transition to a privately-held firm as a potential turning point away from some of those practices—or as an opportunity to expand upon them. In either case, the acquisition is likely to have significant broader implications for the gaming industry. If customers view EA as taking more creative liberties and presenting a more favorable set of mechanics in its games, this could spell trouble for rivals in the industry. Perhaps more likely, though, is the reality that EA will take on about $20 billion of debt in the acquisition process, and that this may drive it to double down on its revenue-generating approaches. If investors take a bearish view of EA's capacity to continue to win fans as it goes private, it may be worthwhile to look at competitors like Take-Two or Roblox. Take-Two enjoyed a strong earnings beat over the summer and impressive net bookings of more than $1.4 billion, and it is expected to launch the highly anticipated next game in the immensely popular Grand Theft Auto series in the coming quarters. Roblox noted impressive revenue growth of 21% year-over-year for the latest quarter as bookings, daily active users, and engaged hours all climbed. Both TTWO and RBLX shares have broad support from a majority of analysts who have rated them a Buy, making them worthwhile considerations for investors attempting to play the ongoing shift in the gaming industry as the EA deal continues to take shape.  Read This Story Online Read This Story Online |  Private deals don't wait for headlines. They move quietly—and often deliver the kind of returns the public markets can't match.

Our new 2025 Accredited Investor Playbook reveals where insiders are placing capital right now. 👉 [Check Your Eligibility & Access the Report] |

| Written by Thomas Hughes

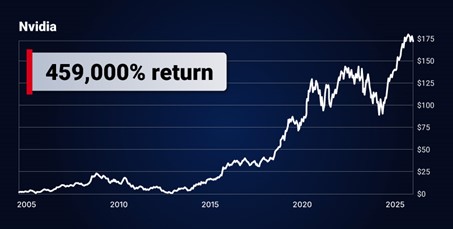

The onset of Q3 earnings season is just around the corner, and it looks like it will be a good one. Not only is there an outlook for S&P 500 (NYSEARCA: SPY) earnings growth and sequential acceleration to follow, but the forecasts are also improving, providing a lift for market spirits. As of early October, the consensus for the year is for earnings to grow by 8.0%, an 80-basis-point improvement from the lows of the revision cycle, and the forecast for the following year is also improving. Three sectors are setting the pace for Q3 earnings growth—and could drive index gains into Q4. Tech, energy, and financials are leading the charge, supported by strong forecasts and key macro tailwinds. But with expectations running high, even solid results could trigger volatility. In a market priced for strength, the risk of a pullback on "good enough" earnings remains. The AI Trade Continues to Gain Momentum The revision trends reveal that the AI trade is alive and well and gaining momentum in the fourth quarter. The consensus figure for the Technology Sector’s (NYSEARCA: XLK) earnings growth is not only the most robust at up 21%, but the revisions are also the hottest. The consensus is up approximately 550 basis points since the cycle low and is likely to continue higher. The primary driver is NVIDIA (NASDAQ: NVDA), which has seen 95% of its analysts increase their earnings estimates over the preceding 90 days, and is expected to grow its earnings by another 50% or more. Also driving the technology sector outlook are Microsoft (NASDAQ: MSFT), Apple (NASDAQ: AAPL), Broadcom (NASDAQ: AVGO), and Oracle (NYSE: ORCL), whose analysts are also lifting earnings estimates. Collectively, including NVIDIA, they represent 50% of the Information Technology Sector and a comparably large portion of the S&P 500. The XLK index is trending higher ahead of the peak reporting season and is likely to continue advancing as the year progresses. However, investors may exercise caution due to the advanced nature of the rally. The market has increased by more than 55% since the last major correction, so it could pull back at any time. Additionally, divergence in the MACD indicates that the rally has weakened, setting the stock price up for potential profit-taking and consolidation that could begin soon, regardless of the strength of Q3 earnings.

Utilities: AI Is Electrifying Growth AI companies are increasing their power consumption daily, driving global electricity demand. At the same time, EV demand is growing, and utilities are investing in modernization and infrastructure to support it. The key takeaway is that the rate base is growing for this sector while rates are increasing, providing a lever for growth. The impact on the earnings outlook is that the Utilities Sector (NYSEARCA: XLU) is forecast to post the second-strongest growth this reporting cycle, and estimates are rising. Up more than 225 basis points since the start of Q3, the consensus figure for the Utilities sector is +18%, led by companies including Constellation Energy (NASDAQ: CEG). It is forecast to grow its earnings by more than 15% with nearly 60% of its analysts having lifted their target during the reporting period. The Utilities Sector ETF is also trending higher, having reached new highs in early October. The move is likely to continue, driven by earnings strength and capital returns; however, investors should remain cautious. Technical conditions, including a diverging MACD and an overbought stochastic, suggest that this market could pull back at any time.

Dual Tailwinds for Financial Stocks The Financial Sector (NYSEARCA: XLF) is forecasted to have grown by 11.5% in Q3, driven by lingering NII strength tied to higher interest rates and consumer resiliency. The forecasts for this sector are also rising, with the consensus up by 400 basis points from its low at the start of the period. The leading stocks in this group include Berkshire Hathaway (NYSE: BRK.A) and JPMorgan (NYSE: JPM), which are well-suited to benefit from the application of AI. On the one hand, Berkshire is a massive insurance company that utilizes AI analysis and automation throughout its network. On the other hand, JPMorgan is the world’s largest financial institution outside of China, and it is planning to become the first fully AI-assisted bank globally. The XLF ETF is also trending higher, poised to make a move that the upcoming earnings reports are expected to catalyze. The likely outcome is a move higher, but once again, this market exhibits some signs of weakening that could result in a price correction or extended consolidation if the results fail to impress the market.

Read This Story Online |  Backed by Jeff Bezos, Bill Gates, and even early Nvidia investors, one little-known AI company — founded by an ex-Google visionary — could be on the verge of unlocking a $27 trillion windfall, and Alexander Green himself is already an investor. Get the full rundown from Alex now |

| Written by Thomas Hughes

As the AI arms race accelerates, Advanced Micro Devices (NASDAQ: AMD) is gaining ground in a market long dominated by NVIDIA. Its recent deal with OpenAI adds weight to the view that AMD stock could still double in value. But this isn’t about taking share from NVIDIA (NASDAQ: NVDA)—analysts at Wedbush estimate demand is outstripping supply by ten to one, creating room for both companies to thrive. AMD’s opportunity lies in meeting a massive unmet need in the AI GPU market. The critical takeaway is that OpenAI wants billions, tens of billions to be more precise, worth of MI450 GPUs. This is important because the MI450 lineup is explicitly tailored for AI workloads, features superior memory capacity suitable for inference, is more efficient, and is available at scale. It is the scale that matters, as hyperscalers will drive revenue growth. Now that AMD’s products are on the verge of launching and have been endorsed by OpenAI, investors may expect to see other leading hyperscalers follow suit. Companies ranging from Amazon (NASDAQ: AMZN) to Alphabet (NASDAQ: GOOGL), Microsoft (NASDAQ: MSFT), and Oracle (NYSE: ORCL) will line up to buy chips in this scenario, driving a boom similar to NVIDIA's for Advanced Micro Devices. Advanced Micro Devices Revenue Outlook Ballooned on OpenAI Deal The impact on revenue growth will be enormous. The deal with OpenAI alone is worth an estimated 100% of the fiscal 2026 earnings outlook and is likely to be the first of many large-scale orders. Not only will hyperscalers that provide public-facing services be clients, but so will any business, organization, or country in need of advanced AI computing power. The takeaway is that Advanced Micro Devices' revenue will begin to skyrocket as soon as the first quarter of availability, likely to exceed 100% year-over-year each quarter for at least the following four and potentially for longer. The impact on analysts' sentiment is also bullish for the market. Not only should investors expect to see analysts lifting their revenue and earnings targets, but outperformance is likely relative to the consensus and will drive market euphoria. The initial response is very bullish, including numerous price target increases and at least one upgrade within the first 24 hours of the release. The upgrade is from Jefferies, which also lifted its price target to $300, the highest on Wall Street. Analysts at the firm believe the OpenAI deal could unlock up to $100 billion in revenue over the next four years. Analysts at Piper Sandler agreed, calling the agreement highly accretive and forecasting well over $100 billion through October 2030. Assuming that AMD maintains its strength relative to forecasts, as NVIDIA has done, the trend in analyst sentiment is likely to continue driving this market, potentially pushing it well above $300.

Advanced Micro Devices Offers a Deep Value at $200 Advanced Micro Devices' earnings growth is also a factor in the share price outlook. The company’s earnings are likely to grow at an accelerated pace, similar to NVIDIA's, outpacing the forecasts that already imply significant value, even when trading at $210. The forecast following the release has AMD stock in the low double-digit P/E range as of 20230 and may be cautious, suggesting its stock price could increase by 100% to 200% within the next few years. If NVIDIA is to be used as a guide, its revenue and earnings forecasts have been blossoming for over two years, and it continues to outperform and provide robust guidance. Its revenue has grown by nearly 1000% in the four-year stack, with earnings increasing at an accelerated pace, a figure that AMD may easily surpass. The demand for inferencing is tied to the application of AI, which is expected to be a far larger industry than the infrastructure industry. The Technical Outlook: Advanced Micro Devices Is at an Inflection Point AMD's share price surged more than 30% following the OpenAI deal, only to hit resistance at the all-time high. The stock surge may pause at this level, but is likely to continue higher before the end of the year due to the improved and still improving outlook, as well as its impact on analysts' sentiment. The critical resistance point is the existing high at $227.30; a move above that will signal a significant shift in market dynamics. The market for AMD stock could advance as much as $130 in a matter of months in this scenario, topping out near $360 sometime in early to mid-2026. Read This Story Online |  Louis Navellier is one of Wall Street's most respected money managers — overseeing more than $7 billion and earning a reputation for fact-based analysis, not sensationalism. That's why his latest economic warning is turning so many heads.

In his new report, Louis reveals how recent policies are accelerating a massive economic shift. While headlines point to strong numbers, everyday Americans feel the squeeze as prices climb and industries are reshaped. According to Louis, this transformation could determine who falls behind — and who builds lasting wealth. Read Louis Navellier's urgent report here |

| More Stories |

| |

|

|