| Written by Jordan Chussler

My identity was stolen once, and that was about as fun as it sounds. After returning from a trip abroad, I noticed a series of errant charges on my credit card statement, including a handful of sneaker stores across Tokyo. That immediately seemed off. At that juncture in my life, I only wore flip-flops, and the closest I’d ever been to anything resembling Japan was my favorite late-night sushi bar. Unfortunately, I’m hardly alone: 22% of Americans report being victims of identity fraud, and 73% of those involve financial identity theft. So protecting our sensitive information has become a big business. However, protecting the sheer volume of big businesses’ sensitive information has become an even bigger business. Grand View Research said the cybersecurity market was worth $246 billion last year. By 2030, it’s projected to double to $500 billion. That’s attributed to heightened demand in a world with an increasing number of cyberattacks, ever-expanding adoption of e-commerce platforms, and a proliferation of smart devices, which has resulted in people becoming more reliant upon mobile financial transactions. North America was the largest market in 2024, but the Asia Pacific is the fastest-growing market. For those who want to invest in this trend, one ETF provides exposure to a basket of the information technology sector's leading global cybersecurity firms by mirroring an index that tracks their performance. AI’s Emerging Role in Cybersecurity Underscoring the need for these services is a common theme over the past several years: AI. With the technology becoming commonplace, the need for innovative cybersecurity applications has arisen, making highly integrated systems that are adaptive, multi-layered, and self-learning imperative. The good part is that the firms offering these services increasingly turn to AI themselves. The other side of that coin? Cybercriminals are, too. As a result, AI has become a double-edged sword for the industry, creating demand for preventative and enhanced defenses such as predictive threat intelligence and automated breach containment. On the other hand, the more sophisticated AI becomes, the more likely it will be to empower and incentivize cybercriminal activity through attacks involving malware and ransomware deployment. A study published earlier in September by MIT Sloan and Safety Security found that, of the 2,800 ransomware attacks it reviewed, 80% were powered—to some degree—by AI. Global enterprises now typically commit between 10% and 20% of their IT budgets strictly to cybersecurity. But those services aren’t just needed by individuals and companies. Governments around the world are increasingly reliant on Big Data, which in turn is fueling spending that supports cybersecurity market growth. For example, by the end of 2025, the U.S. federal government will have doled out $13 billion to combat this growing threat. An All-Star Lineup of Cybersecurity Firms For investors who want a piece of this growing pie, the Global X Cybersecurity ETF (NASDAQ: BUG) is an all-in-one solution. While a 0.51% expense ratio may be on the higher side for a passively managed fund, BUG provides exposure to a veritable who’s who of the cybersecurity industry, with its top five holdings including: The fund is well-balanced; those five positions account for over 30% of the portfolio. In total, 25 total holdings spanning countries such as the United States, Israel, Japan, Canada, and South Korea aim to replicate the performance of the Indxx Cybersecurity Index. That has worked out well since its inception on Nov. 1, 2019. Since then, the BUG has been up 122.58% while paying a modest dividend that currently yields 0.08%. Its performance as of late has been far more impressive, though. Since its five-year low on Jan. 6, 2023, the fund has been up more than 75%, including a nearly 19% gain from its year-to-date low in April. What the Smart Money Thinks Wall Street seems to be attuned to the growing demand for cybersecurity services. Institutional buyers (134) have outnumbered institutional sellers (72) over the past 12 months. Although volume can be light, inflows of nearly $198 million have surpassed outflows of $63 million by a sizable margin over the same period. At the same time, short interest is a mere 0.73% of the 32.7 million shares outstanding. While the BUG isn’t exactly illiquid, the average daily trading volume of 286,744 is something to be mindful of. But if you’re for a buy-and-hold broad play for cybersecurity, this ETF has far more to like than dislike.  Read This Story Online Read This Story Online |  While many are busy chasing the usual AI trends, a bigger opportunity is quietly brewing—and most are missing it. Imagine a major shift in how and where AI is built, opening up incredible wealth opportunities for those in the know.

I've found 9 AI companies primed to lead this change. These aren't the tired "AI hype" stocks; they're companies with real US operations, proven revenue growth, and deep AI integration. I've put all the details in a FREE report: "Top 9 AI Stocks For This Month." |

| Written by Thomas Hughes

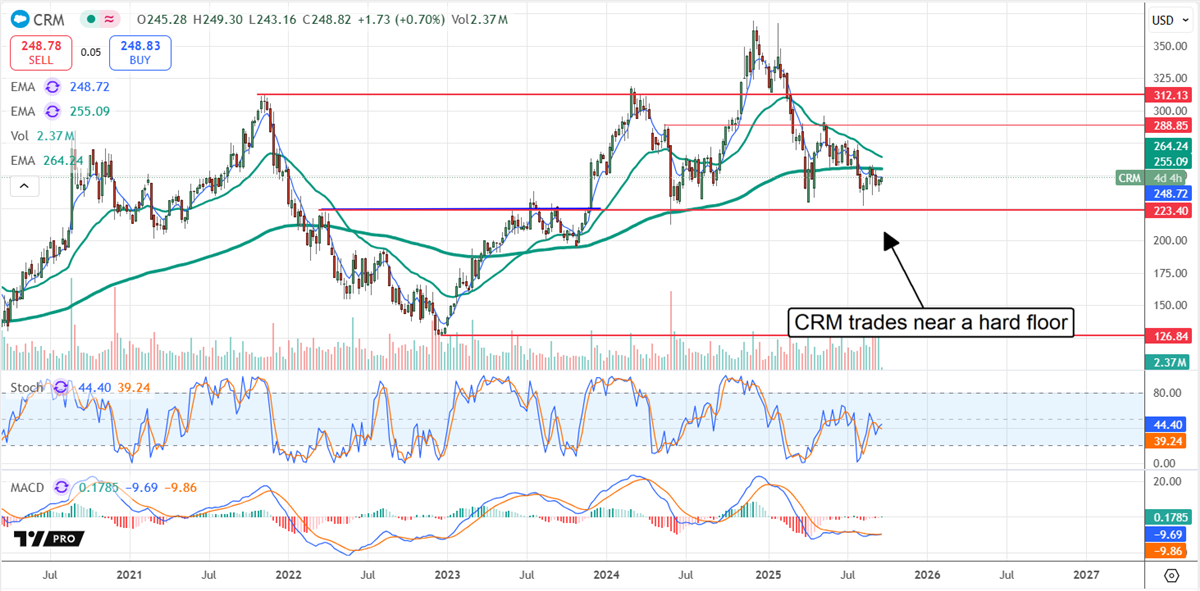

Analysts' sentiment and downgrades can significantly impact a stock price, helping it to correct or even sustain downtrends despite otherwise bullish indications. The main point to remember is that downgrades and price target reductions are generally based on the overall market conditions. Bearish analyst activity within a downtrend of activity will sustain a downtrend in price action, while bearish activity within an otherwise bullish market can open up significant buying opportunities. This article focuses on three low-priced stocks that recently appeared on the list of Most Downgraded Stocks and offer investors opportunities with long-term potential. Analysts' sentiment impacts the action today, but the sell-offs are overdone and price rebounds are just around the corner. Salesforce Ranks High on the List of Most Downgraded Stocks: It’s a Hot Buy Salesforce’s (NYSE: CRM) analyst activity in 2025 is sufficient to rank it highly on MarketBeat’s list of Most Downgraded stocks. However, the bearish activity is relative; the 38 analysts tracked provide solid support, rating the stock as a Moderate Buy with a bullish bias. The bias is robust, with 72% rating as an outright Buy and the consensus price target forecasting a 35% upside as of late September. Most of the bearish activity has been driven by price target reductions; importantly, these reductions align with the consensus and the low-end range that acts as a technical price floor. The low end of the analyst range is $221, a level that has been tested as support several times in the past. The likely outcome is another rebound from this level, which could run from 10% to 25% within a few weeks. Another factor suggesting a rebound is likely is institutional activity, which has been bullish every quarter this year. The group owns over 80% of the shares and is unimpeded by short-selling activity. Short-sellers are present, but the low 1.5% interest is negligible. CRM's growth outlook, cash flow, dividend, and share buybacks make it a potential buy for long-term investors. The company may not be inspiring analysts and the market to rally. Still, it is growing and sustaining a solid pace, producing ample cash flow, paying a dividend with expected distribution growth, and reducing its share count. The last report included a 1.1% share count reduction and authorization increase, assuring the pace will continue for the foreseeable future.

CrowdStrike’s Analyst Trends Are Reinvigorated CrowdStrike’s (NASDAQ: CRWD) 2025 analyst activity is sufficient to place it on the list of Most Downgraded names, but the data also reveals a shift that is pushing the market higher. The post-release activity includes numerous price target increases, which have CrowdStrike on the Most Upgraded List simultaneously as the Most Downgraded, and the price targets are aggressive. The consensus assumes the market is at fair value near $490, but the latest revisions put the stock in the high-end range, which provides another 15% upside. Institutional support is helping this market move higher. The group owns over 70% of the stock and has been buying all year. The balance is more than $2-to-$1 in favor of buyers, providing a strong tailwind. The next visible catalyst is the calendar Q3 earnings report due in late November. Given the cybersecurity and AI industry trends, the company issued strong guidance due to AI and will likely exceed its outlook.

Fortinet: Correction Over, Recovery Underway Fortinet’s (NASDAQ: FTNT) stock price imploded in Q3 following an otherwise bullish report in which growth was above expectations, but the future came into question. Analysts believe the firewall upgrade cycle may be half or more completed, suggesting tepid growth in the upcoming years. However, with AI gaining momentum, Fortinet is well-positioned as cybersecurity will become increasingly essential and evolve to meet increasingly intelligent attacks. Analysts rate Fortinet as a Hold with a bullish bias. The bias isn’t robust; only 27% rate as a Buy, but the coverage is increasing. The number of analysts covering the stock increased by three from August to September, indicating a stronger support base, if not a tailwind, for the action. The institutions are likewise supportive, owning more than 80% of the stock and buying on balance every quarter this year. Fortinet does not return significant amounts of capital to its shareholders; instead, it reinvests in the business to build equity. Equity reverted from negative to positive in F2204 and grew by nearly 38% in the first six months of fiscal 2025.

Read This Story Online |  One trader turned a $1.20 NVDA option into a 108% gain—on just a 3% move.

Forget what you've heard about options. This underground setup lets traders target 100%+ gains on popular stocks using dirt-cheap contracts—no big moves or big accounts required. See how this rebel strategy beats quiet markets |

| Written by Dan Schmidt

The cryptocurrency rally has taken a backseat to new all-time highs in the major U.S. market indices, but that doesn’t mean enthusiasm for digital assets has faded. In fact, Wall Street has gone beyond its embrace of Bitcoin by welcoming other tokens into the fold, like Ethereum and Solana. Ethereum has outperformed Bitcoin by approximately 5% year-to-date; however, the altcoin rally has been far more pronounced over the last three months. What’s causing these secondary cryptos to rally beyond Bitcoin? We’ll answer that question today and discuss three stocks of interest that saw the Solana rally coming. Why Solana Surged Ahead in the Cryptocurrency Markets Solana is by no means a small fish in the crypto pond, but it's been a distant third to Bitcoin and Ethereum, which have been hogging Wall Street’s attention for most of the year. Bitcoin ETFs and treasuries are now commonplace on U.S. exchanges, and the success of companies like Strategy Inc. (NASDAQ: MSTR) has led others to enter the crypto treasury business. Public companies treat Bitcoin like digital gold, and so far, investors have been more than willing to pay up for stocks with significant Bitcoin holdings. If Bitcoin were gold in this scenario, Ethereum and Solana would be more like oil or soybeans. ETH and SOL are platforms that can be used to build ecosystems for NFTs or decentralized finance projects, but they can also earn yield. We discussed Ethereum treasury strategies last month, and Solana strategies are being enacted similarly. Solana backers claim several advantages over the Ethereum platform, such as: - Faster transfer speeds (up to 1000 transactions per second)

- Lower and more stable transaction fees

- Double the average yield on Ethereum

That last bullet is crucial; while Solana is more volatile than its larger brethren, the ability to earn higher yields makes it attractive to small-cap stocks looking to transition their business into crypto treasuries. And suppose you’re a small-cap in the competitive tech sector with minimal revenue growth. In that case, you probably don’t mind a little volatility, mainly when the market narrative works in your favor. Solana has outperformed Bitcoin and Ethereum over the last month, and investors have handsomely rewarded the stocks of companies that began stacking SOL tokens in the previous quarter. 3 Small-Cap Stocks That Loaded Up on Solana Like the Ethereum treasury companies, these three small caps began accumulating SOL tokens to bolster their underlying businesses. If you’re looking for fundamentally sound stocks with proven business models and strong revenue growth, you’re barking up the wrong stock sector tree. These companies are speculative plays meant for trading, not long-term investments, so make sure your risk tolerance and goals are aligned before taking on new positions in them. Forward Industries: The Largest Public Solana Treasury Forward Industries Inc. (NASDAQ: FORD) has become the biggest public SOL holder, amassing more than 6.8 million tokens as of Sept. 15. The company’s primary businesses are manufacturing custom cases for high-value merchandise and customer electronics, and rallying when novice investors mistake its stock for Ford Motor Co. (NYSE: F). However, this pivot to Solana has been profitable for investors, and the stock has been up more than 450% year-to-date (YTD) and 160% in the last month alone. Forward Industries earned about $30 million in total revenue in 2024, a year-over-year (YOY) decline of more than 17%. The company’s Q3 2025 revenue figure was just $2.49 million, a paltry showing compared to the $7.89 million generated in Q3 2024. The primary business has been struggling, so FORD executives have little to lose by switching to a volatile crypto treasury strategy. The stock is also down 16% in the last five days, offering a potential entry point. DeFi Development Corp: A Natural Fintech Pivot Formerly Janover Inc., DeFi Development Corp. (NASDAQ: DFDV) was a B2B fintech marketplace before moving into cryptocurrency. But Janover was a penny stock trading under $1 per share since June 2024, and its SOL treasury initiatives sent the stock from 57 cents to $42 in just six weeks. Yes, you read that right: 57 cents to 42 whole dollars. DFDV shares have fallen significantly from their May highs, declining 37% over the past three months. However, the company still holds about two million SOL, and it received coverage from Cantor Fitzgerald in August, which rated it as a Strong Buy. Upexi: Utilizing Solana to Expand Core Business Upexi Inc. (NASDAQ: UPXI) is ‘only’ up about 70% YTD, and has cratered more than 20% in the last month. The company’s digital consultancy business grew its annual revenue from $7.4 million in 2020 to $36.4 million by 2023. However, sales declined nearly 30% in 2024, and its latest Q1 2025 earnings release showed just $3.16 million in quarterly revenue. The company adopted a SOL treasury strategy to boost this revenue stream and purchased just over two million tokens earlier this year. Unlike FORD and DFDV, Upexi plans to utilize its SOL holdings as a supplementary revenue source and continue to build its primary business by helping companies market and launch new products. Read This Story Online |  Something unusual is happening inside a 40-person crypto research firm.

They're helping 8,000+ ordinary people pull consistent profits from crypto — not through luck or timing, but through a systematic approach with a documented 93% win rate. Claim Your Free Trade Setup → |

|